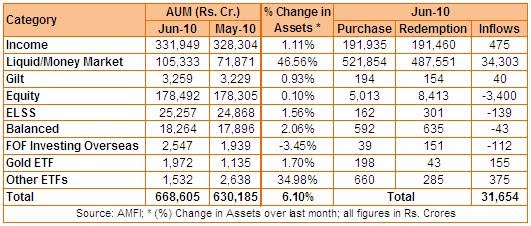

Mutual Fund industry saw a temporary relief after witnessing outflows in last two months consecutively. In July 2010, the industry saw a net inflow of Rs. 31,654 crore to its kitty mainly on account of net inflow of Rs. 34,303 crore in Liquid/Money Market category. On the other hand, the total AUM increased to Rs. 6.68 lakh crore, a rise of Rs. 38,420 crore or 6.10 per cent over the last month figure. All categories except FOF Investing Overseas reported an increase in its net AUM. While Income Funds comprising 50 per cent of total AUM reported a meager increase of 1.11 per cent in its AUM, Liquid/Money Market Fund category reported an increase of 46.56 per cent. The latest AUM figures for Income and Liquid/Money Market Fund stand at Rs. 3,31,949 crore and Rs. 1,05,333 crore respectively. The Other ETFs category shows a dramatic increase in AUM after Motilal Oswal Mutual Fund successfully closed its maiden fundamentally modified ETF MOSt Shares M50 with a total AUM of Rs. 236 crore. It has a total AUM of Rs. 1,532 crore, an increase of Rs. 397 crore other its last month figure. The Diversified Equity category showed a negligible increase of 0.10 per cent to Rs. 1,78,492 crore. Other categories too moved up albeit marginally.

The Equity Diversified Fund category saw a major redemption having a total outflow of Rs. 8,413 crore against an inflow of Rs. 5,013 crore, thus, a net redemption of Rs. 3,400 crore. The equity markets have already touched their February 2008 level and investors have become cautious of overheat going in the equity market as they fear a correction from this level. Moreover, some investors who were sitting at their investment since 2007 had also redeemed their money. Hence mutual funds booked profit to meet investors’ redemption pressures. As per the latest SEBI figures, Mutual Funds had net sale of Rs. 4,405 crore in July 2010.

|

| Table: Mutual Fund Asset Growth |

The Liquid/Money Market saw the maximum inflow of Rs. 34,303 crore mainly on account of switch outs from Income/Ultra Short Term Funds to Liquid Funds. After the introduction of new MTM ruling on debt securities having average maturities more than 91 days, the Ultra Short Term Funds were the worst hit. Corporate fears that it will bring volatility to the funds which will bring down the returns. They eventually shifted to Liquid Funds or redeemed their investments. The Income category saw a net inflow of Rs. 475 crore only.

In other categories, ELSS saw a new outflow of Rs. 139 entering into fourth month having outflows consecutively month-on-month. Balanced Funds too saw an outflow of Rs. 43 crore continuing its last month losing streak. However, the industry has been witnessing a major shift since last few months from active funds to passive funds. ETFs which cater to passive funds category have seen a substantial increase in inflows. The Gold ETF and other ETFs category added Rs. 155 crore and Rs. 375 crore respectively.

The month also saw the launch of 7 open-ended NFOs and 15 close-ended NFOs (mainly FMPs). The 15 close-ended income funds collected Rs. 2,444 crore from the market while the 3 open-ended close ended funds collected Rs. 840 crore. The income category NFOs were Axis Income Saver, Canara Robeco InDiGo Fund and Peerless Income Plus Fund. The 2 open-ended Equity NFOs, mainly Mirae Asset Emerging Bluechip Fund and SBI PSU Fund collected a total of Rs. 705 crore. In other ETFs category, Motilal Oswal MOSt Shares M50 ETF collected Rs. 236 crore in its maiden NFO.

Source: MOSL Mutual Fund Desk