In the 21st century, the women share a new power statistics ruling almost every domains of life. Worldwide, different governments have given different reservations to motivate them to come at par with their men counterparts. Throughout history, women and nature have been closely linked. Also the idea of “mother earth” is common to many Indo-European cultures. Even in the current Bihar election (2010) where the NDA regime (JD-United and BJP) thwarted its opposition by an unprecedented margin, the women voters played an important role in affecting the political economics.

Moreover, the financial crisis has defined a new power shift from West to East. In industrialized economies, the availability of high quality forms of energy has greatly reduced the amount of time and effort that women must dedicate to housework. Nonetheless, there is substantial evidence that women are more sensitive to environmental matters.

Read more on Women nurturing sustainable development – remarks by Anna Maria Tarantola, Deputy Director General of the Bank of Italy. The paper explains the relationship between women and the environment in developing countries including The Industrial World: A green economy led by women.

Happy Reading!

- Amar Ranu

November 26, 2010

November 22, 2010

Macro-prudential policy: Asian Perspective

Macro-prudential policy has become a norm after the outbreak of global financial crisis. The international bodies such as IMF and the Financial Stability Board (FSB) stated clearly that implementing macro-prudential policy should be central banks’ responsibility. It is a new concept and counter cyclical.

Read more on the opening remarks at the High Level Seminar of “Macro-prudential policy: Asian Perspective”…

Happy reading!

- Amar Ranu

Read more on the opening remarks at the High Level Seminar of “Macro-prudential policy: Asian Perspective”…

Happy reading!

- Amar Ranu

November 18, 2010

Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo Approach

The world had been overleveraging in pre-financial crisis. Post Lehman scathe, there has been talks of deleveraging and the liquidity including debt which seem like a trap again. Paul Krugman from Princeton University and Gauti B. Eggertsson (NeyYork Fed) talk about Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo Approach.

The approach sheds considerable light both on current economic difficulties and on historical episodes, including Japan’s lost decade (now in its 18th year) and the Great Depression itself.

Read more…

The approach sheds considerable light both on current economic difficulties and on historical episodes, including Japan’s lost decade (now in its 18th year) and the Great Depression itself.

Read more…

November 10, 2010

Aiding the economy: What the Fed did and why

Aiding the economy: What the Fed did and why?

For a quite long time, all the economies have been struggling to keep pace or evolve after the worst financial crisis (last we had in 1930s). More monies were pumped into throughout the world amounting into trillion of dollars - US had QE-I followed by QE-II and various other measures by other countries too.

QE II may be a fait accompli but the Fed Governor justifies it citing the high unemployment rate and low inflation. Read his opinion Aiding the economy: Why the Fed did and why

Enjoy reading!

For a quite long time, all the economies have been struggling to keep pace or evolve after the worst financial crisis (last we had in 1930s). More monies were pumped into throughout the world amounting into trillion of dollars - US had QE-I followed by QE-II and various other measures by other countries too.

QE II may be a fait accompli but the Fed Governor justifies it citing the high unemployment rate and low inflation. Read his opinion Aiding the economy: Why the Fed did and why

Enjoy reading!

November 5, 2010

12th March – a reason to rejoice or lament

The 12th March has always been an unforgettable day in my life – not for the reasons I am born blissfully on this day to my proud parents to whom I cannot return my duties but it will always be remembered for the barbaric crime done on Indian soil. The reasons – avenge; a thirst to kill each other which the British rulers successfully imbibed into us. Yes, I am talking about the non-ending story of Hindu – Muslim dilemma where the chapter of Babri Masjid, Mumbai’s Serial Bomb Blasts, Gujarat riots and riots post Babri Masjid’s demolition were red lettered.

I always wonder – should I celebrate my most important in my life where every year I lose an important year or should I go ahead without remembering those who were either killed or wound permanently in the Mumbai’s serial blast of 12th March 1993, the Black Friday in Mumbai History. Recently I happened to read the book “Black Friday – The True Story of the Bombay Bomb Blasts” by S. Hussain Zaidi. Though it was out for public circulation in 2002, I happened to read it in recently. It was better than sure that the events had been an avenge to Babri Masjid’s demolition post which Muslims were butchered albeit Hindus were also killed. The book also described the involvement of Sanjay Dutt, the Bollywood star and the son of MP and another Bollywood veteran, Shri Sunil Dutt, who had nothing to do with Bomb Blast and had procured an AK 56 in curiosity to defend himself after he was threatened from pro-Hindu fundamentalists. I still wonder how he thought of defending himself after he was threatened from fundamentalists as he showed some good friendly gestures to Muslims’ communities after Bombay’s riots of Dec 1992 and Jan 1993.

The book also describes the heroic efforts put by Mumbai Police and its network. Now I believe why it is named after Scotland Yard in its service and work-style. Its nexus with dons, bhais, bollywood stars and many unrecorded relations, also known as informants made it one of the strongest Bhai of aamchi Mumbai. Mr. Rakesh Maria, Deputy Commissioner of Police (Traffic) and the then in-charge of Bombay’s Bomb Blasts in 1993 and now the Joint Commissioner of Police and also investigated the recent Mumbai’s Terror Attack of 2008 really deserve a pat. He handled both the cases in a very intuitive way.

While India leaves behind its story and Mumbai goes forward in its spirit, there are some people who try to erase their past memories but unable to do so.

I must think on – should I still go ahead in celebrating my birthday with a big bang where I extinguish my candle or should I light a candle in the memory of those who were directly or indirectly killed or wound and their life are still a challenge for them. Let someone answer this million dollar question!

Hats-off to the spirit of Mumbai! I love it.

I always wonder – should I celebrate my most important in my life where every year I lose an important year or should I go ahead without remembering those who were either killed or wound permanently in the Mumbai’s serial blast of 12th March 1993, the Black Friday in Mumbai History. Recently I happened to read the book “Black Friday – The True Story of the Bombay Bomb Blasts” by S. Hussain Zaidi. Though it was out for public circulation in 2002, I happened to read it in recently. It was better than sure that the events had been an avenge to Babri Masjid’s demolition post which Muslims were butchered albeit Hindus were also killed. The book also described the involvement of Sanjay Dutt, the Bollywood star and the son of MP and another Bollywood veteran, Shri Sunil Dutt, who had nothing to do with Bomb Blast and had procured an AK 56 in curiosity to defend himself after he was threatened from pro-Hindu fundamentalists. I still wonder how he thought of defending himself after he was threatened from fundamentalists as he showed some good friendly gestures to Muslims’ communities after Bombay’s riots of Dec 1992 and Jan 1993.

The book also describes the heroic efforts put by Mumbai Police and its network. Now I believe why it is named after Scotland Yard in its service and work-style. Its nexus with dons, bhais, bollywood stars and many unrecorded relations, also known as informants made it one of the strongest Bhai of aamchi Mumbai. Mr. Rakesh Maria, Deputy Commissioner of Police (Traffic) and the then in-charge of Bombay’s Bomb Blasts in 1993 and now the Joint Commissioner of Police and also investigated the recent Mumbai’s Terror Attack of 2008 really deserve a pat. He handled both the cases in a very intuitive way.

While India leaves behind its story and Mumbai goes forward in its spirit, there are some people who try to erase their past memories but unable to do so.

I must think on – should I still go ahead in celebrating my birthday with a big bang where I extinguish my candle or should I light a candle in the memory of those who were directly or indirectly killed or wound and their life are still a challenge for them. Let someone answer this million dollar question!

Hats-off to the spirit of Mumbai! I love it.

November 2, 2010

Infrastructure Funds – poised to grow

A robust infrastructure; ask any individual he will define or relate it. Infrastructure has become a new catchphrase in India with more government allocations, both through policy reforms and increased spending. This has been well emphasized in Budget 2010 where a massive Rs. 1,73,000 crore or 46 per cent of total plan was allocated to infrastructure only. Infrastructure augments the growth of Indian economy and India’s economic growth has been attracting wide attention. The International Monetary Fund (IMF) has come out to state that Indian economy will grow at 9.7 per cent in FY 2010 and 8.4 per cent in FY 2011. The economy is on the fulcrum of an increasing growth curve; thus, economic prosperity is placing huge demands on infrastructure. It is attributed that India’s submissive infrastructure is the key reason for the country not achieving double digit GDP growth.

Though the Government of India has been addressing the infrastructure requirements, the pace of growth has been lacking.

Infrastructure – Has it performed well?

While Infrastructure has been defined differently from different Portfolio Managers, we have considered sectors such as Telecom, Consumer Goods, Utilities – Gas and Power, Real Estate, Petroleum and Gas, Engineering as basic components of Infrastructure (combining all the definitions as per different Offer Documents of Infrastructure Funds). Banks have also found a prominent place in major of the funds; so, we would also consider it.

Indian equity markets have delivered superb performance in the last quarter including CYTD , thanks to increased capital inflows and extended quantitative easing in developed countries which have forced cheap money to move into emerging markets including India too. India has emerged as the best performing market globally and is poised to be one of the earliest to scale its previous peak and create new highs. From peak of CY 2007-08, major sectoral movers are Auto, PSU-Banks, FMCG, Pharma and IT moving in the range of 39 to 71 per cent while the Engineering, Petroleum and Gas, Utilities, Telecom and Real Estate – which comprise predominantly Infrastructure have underperformed in the range of (-) 21 to (-) 72 per cent.

Does it say that the infrastructure story is over in India?

If we believe the 11th Five Year Plan (2007-2012), it calls for more than doubling the financial outlay for infrastructure. The investments will touch US $ 1.48 trillion by 2017. Some of the major developments in the past such as world class airports, flyovers, CWG Event which helped in creating world class sporting complexes (barring inappropriate use of funds) have proved to be the major boost to Infrastructure in the near future.

Similarly, we are on Capex boom (dhoom) driven by impending large investment in infrastructure and industrial activity. India is among leading global destinations for infrastructure and investment spending over the next decade. Sectors which have shown growth rates consistently over the last six quarters are Engineering, Banking, FMCG and IT. However, telecom continues to post its fifth consecutive quarter of earnings decline. We believe that the 2HFY11 will have changed growth pattern across sectors like Cement, Engineering, Real Estate, Infrastructure, Utilities reporting better earnings growth than they did in the past. Telecom will continue to post negative earnings growth for 2HFY11. As per MOSL estimates as given below, Engineering and Real Estate are poised to report better quarterly earnings growth in 2HFY11 at 31.8 per cent and 47.2 per cent against the 2Q10 estimates of 17.3 per cent and -1.5 per cent respectively. Infrastructure is also poised to grow at 37 per cent in 4Q10 against 2Q10 figures of 12.6 per cent; ditto with Utilities growing at 15.1 per cent against 8 per cent in 2Q10.

Also, the 2QFY11 earnings for MOSL universe (139 stocks) are more broad-based with 73 per cent of companies (v/s 70 per cent in June 2010) in a positive earnings growth trajectory and vice-versa.

Infrastructure Funds in India – Are they poised to grow?

Mutual Funds in India have been growing through rough patches but are poised to bounce back with a big-bang. The industry has several infrastructure funds to offer – as on Sept 30, there are 21 funds – it includes both open-ended and close-ended. Infrastructure Funds invest in stocks of companies which cover several sectors like petroleum and gas, utilities, real estate, engineering, FMCG etc. Unlike in other thematic funds, they are not restricted to a few sectors. On an average, they manage total assets of over Rs. 18,932 crore as on Sept 30, 2010.

From table 1, it can be seen that infrastructure funds have highest average allocation to Energy (24.64%) followed by Industrial Manufacturing (15.3%), Financial Services (14.92%), Construction (12.64%) and Metals (7.94%).

Performance – muted but poised to grow in future

Infrastructure Funds remained a mute spectator in the current Bull Run. In pre-crisis era, these funds had given a reasonable performance but it underperformed when compared to diversified fund category. As per table 2, it paralleled headline indices’ performance like Sensex and Nifty 50 in bull phase while it underperformed them in bear phase. However, in 5-year category, it outperformed all major categories except Bankex which gave an exception performance.

Among the largest infrastructure funds in terms of assets managed, ICICI Pru Infrastructure Fund, DSP BR TIGER Fund among others have outperformed major indices in 5-year category.

Conclusion

• Despite many hiccups including political unwillingness, infrastructure is sure to pick up in future which will augur well for various sectors like power, construction, engineering, energy, cement etc. It will also bode well for funds with these themes.

• Though riskier than diversified equity funds, investors with higher risk appetite can consider allocating 10-15 per cent of their portfolio to these funds.

• Investors must stick to good performing funds having less volatility and lesser concentration risk.

Source: MOSL

Nov 02 policy review eyed

Highlights:

• Amid tight systematic liquidity, the RBI announced a special second LAF, a liquidity window for scheduled commercial banks to borrow to the extent of up to 1.0 per cent of their Net Demand and Time Liabilities (NDTL) as on Oct 08 on all days during Oct 29-Nov 04, 2010. The RBI also announced a special 2-day repo auction under the LAF on Oct 30, 2010 which saw a total borrowing of Rs. 11,025 crore under LAF. The RBI also allowed waiver of penal interest, if any for any shortfall in maintenance of SLR on Oct 30-31, 2010 out of these special facilities.

• The buy-back programme as announced by the government did not draw good responses from the market – with bids worth Rs. 3,174 crore tendered against the notified amount of Rs. 12,000 crore. However, the total amount accepted for buy-back was Rs. 2,148 crore only.

• The benchmark bond seemed to lose its appetite after volume shifted to 8.13% G-Sec 2022 as the market expected that 7.80% G-Sec 2020 may not see any auctions further. However, comments from a Finance Ministry official who hinted that the 10-year bond will retain its benchmark status till fiscal year end led to a swift rally in it. Further, the RBI’s special liquidity window led to fall in yields. The 10-year benchmark paper closed at 8.11, down by 3 bps over the week.

• India’s primary articles’ inflation fell to 16.62 per cent in the week ended Oct 16 from 18.05 per cent in the last week while food articles’ inflation fell to a 50-week low of 13.75 per cent from 15.53 per cent a week before.

• Growth in India’s key infrastructure industries, which constitute 26 per cent of IIP figures fell to a 19-month low of 2.5 per cent in Sept compared to 3.9 per cent and 4.3 per cent in Aug and a year ago respectively.

View & Recommendations:

• The special liquidity window announced by RBI may ease the structural liquidity crisis. The RBI is looking to normalize policy rates given high inflation; however, it feared that the QE-II (Quantitative Easing 2 to be announced by Fed Reserve) may bring more capital inflows into the system which will force the RBI to contain the rupee appreciation. This may lead to inflation hike further.

• The market participants have expected a hike of 25 bps in policy rates to be announced by RBI on Nov 02. The market has already factored into the 25 bps hike in policy rates. So, yields might not move significantly if there is hike in policy rates. However, the government may decide to cancel the auction after which the government bonds may witness a rally.

Broader Perspectives:

Bond Front

The buy-back programme announced by RBI did not draw strong interests from market participants. Bids worth Rs. 3,174 crore were tendered against the notified amount of Rs. 12,000 crore. However, the total amount accepted for buy-back was Rs. 2,148 crore. The securities which are bought back are 8.75% G-Sec 2010, 12.32% G-Sec 2011 and 6.57% G-Sec 2011 for notified amount of Rs. 28.97 crore, Rs. 616.35 crore and Rs. 1,502.97 crore respectively. The inflation continued to remain in uncomfortable zone which may allow the central bank to use all its ammunitions, policy rate hikes being the most prominent one. The RBI policy will be announced just before the much awaited US Federal Reserve announcement regarding the much touted QE-II, or second round of quantitative easing. The probability goes high as the US jobless rate hovered around 10 per cent for a third month in October.

The benchmark yield kept on spiraling and touched its near months high of 8.18 per cent. Meanwhile, the borrowing limit in benchmark bond saw a shift in active trading to other yields. The 10-year benchmark paper closed at 8.11 per cent, down by 3 bps. The 8.13% G-Sec 2022 became the most actively traded securities during the last week.

The tight liquidity scenario, an example of structural liquidity deficit led to a hike in interbank call money markets which rose as high as 12 per cent. During the week, the banks borrowed a net amount of Rs. 4.80 lakh crore against the previous week of Rs. 3.17 lakh crore. The Repo and CBLO rate closed at 6.43 per cent and 7.96 per cent, an increase by 72 bps and 261 bps respectively.

The 1/10 year G-Sec spreads fell to 112 bps from 124 bps a week earlier. And the average G-Sec volume reported was Rs. 47,412 crore compared to Rs. 53,776 crore a week earlier.

Bond Supply

The market didn’t have any central government auctions scheduled for this week; however, the SDL (State Development Loans) auctions raised Rs. 8,601.8 crore as against the notified amount of Rs. 8,226.8 crore with the state of Tamil Nadu exercising the green show option to the tune of Rs. 375 crore.

Liquidity

The systematic liquidity remained in deficit mode which allowed RBI to open an additional liquidity window. The liquidity as measured by bids for reverse repo/repo in the LAF (Liquidity Adjustment Facility) auction of the RBI reported a net borrowing of Rs. 4,80,180 crore or daily average of Rs. 80,030 crore.

Corporate Bonds

The corporate bond yields saw a hike in the concluding week. The 10-year AAA bond ended at a yield of around 8.80 per cent compared to 8.76 per cent in the previous week. Credit spreads moved up with 5-year AAA spreads moving up by a basis point to 69 bps levels.

• Amid tight systematic liquidity, the RBI announced a special second LAF, a liquidity window for scheduled commercial banks to borrow to the extent of up to 1.0 per cent of their Net Demand and Time Liabilities (NDTL) as on Oct 08 on all days during Oct 29-Nov 04, 2010. The RBI also announced a special 2-day repo auction under the LAF on Oct 30, 2010 which saw a total borrowing of Rs. 11,025 crore under LAF. The RBI also allowed waiver of penal interest, if any for any shortfall in maintenance of SLR on Oct 30-31, 2010 out of these special facilities.

• The buy-back programme as announced by the government did not draw good responses from the market – with bids worth Rs. 3,174 crore tendered against the notified amount of Rs. 12,000 crore. However, the total amount accepted for buy-back was Rs. 2,148 crore only.

• The benchmark bond seemed to lose its appetite after volume shifted to 8.13% G-Sec 2022 as the market expected that 7.80% G-Sec 2020 may not see any auctions further. However, comments from a Finance Ministry official who hinted that the 10-year bond will retain its benchmark status till fiscal year end led to a swift rally in it. Further, the RBI’s special liquidity window led to fall in yields. The 10-year benchmark paper closed at 8.11, down by 3 bps over the week.

• India’s primary articles’ inflation fell to 16.62 per cent in the week ended Oct 16 from 18.05 per cent in the last week while food articles’ inflation fell to a 50-week low of 13.75 per cent from 15.53 per cent a week before.

• Growth in India’s key infrastructure industries, which constitute 26 per cent of IIP figures fell to a 19-month low of 2.5 per cent in Sept compared to 3.9 per cent and 4.3 per cent in Aug and a year ago respectively.

View & Recommendations:

• The special liquidity window announced by RBI may ease the structural liquidity crisis. The RBI is looking to normalize policy rates given high inflation; however, it feared that the QE-II (Quantitative Easing 2 to be announced by Fed Reserve) may bring more capital inflows into the system which will force the RBI to contain the rupee appreciation. This may lead to inflation hike further.

• The market participants have expected a hike of 25 bps in policy rates to be announced by RBI on Nov 02. The market has already factored into the 25 bps hike in policy rates. So, yields might not move significantly if there is hike in policy rates. However, the government may decide to cancel the auction after which the government bonds may witness a rally.

Broader Perspectives:

Bond Front

The buy-back programme announced by RBI did not draw strong interests from market participants. Bids worth Rs. 3,174 crore were tendered against the notified amount of Rs. 12,000 crore. However, the total amount accepted for buy-back was Rs. 2,148 crore. The securities which are bought back are 8.75% G-Sec 2010, 12.32% G-Sec 2011 and 6.57% G-Sec 2011 for notified amount of Rs. 28.97 crore, Rs. 616.35 crore and Rs. 1,502.97 crore respectively. The inflation continued to remain in uncomfortable zone which may allow the central bank to use all its ammunitions, policy rate hikes being the most prominent one. The RBI policy will be announced just before the much awaited US Federal Reserve announcement regarding the much touted QE-II, or second round of quantitative easing. The probability goes high as the US jobless rate hovered around 10 per cent for a third month in October.

The benchmark yield kept on spiraling and touched its near months high of 8.18 per cent. Meanwhile, the borrowing limit in benchmark bond saw a shift in active trading to other yields. The 10-year benchmark paper closed at 8.11 per cent, down by 3 bps. The 8.13% G-Sec 2022 became the most actively traded securities during the last week.

The tight liquidity scenario, an example of structural liquidity deficit led to a hike in interbank call money markets which rose as high as 12 per cent. During the week, the banks borrowed a net amount of Rs. 4.80 lakh crore against the previous week of Rs. 3.17 lakh crore. The Repo and CBLO rate closed at 6.43 per cent and 7.96 per cent, an increase by 72 bps and 261 bps respectively.

The 1/10 year G-Sec spreads fell to 112 bps from 124 bps a week earlier. And the average G-Sec volume reported was Rs. 47,412 crore compared to Rs. 53,776 crore a week earlier.

Bond Supply

The market didn’t have any central government auctions scheduled for this week; however, the SDL (State Development Loans) auctions raised Rs. 8,601.8 crore as against the notified amount of Rs. 8,226.8 crore with the state of Tamil Nadu exercising the green show option to the tune of Rs. 375 crore.

Liquidity

The systematic liquidity remained in deficit mode which allowed RBI to open an additional liquidity window. The liquidity as measured by bids for reverse repo/repo in the LAF (Liquidity Adjustment Facility) auction of the RBI reported a net borrowing of Rs. 4,80,180 crore or daily average of Rs. 80,030 crore.

Corporate Bonds

The corporate bond yields saw a hike in the concluding week. The 10-year AAA bond ended at a yield of around 8.80 per cent compared to 8.76 per cent in the previous week. Credit spreads moved up with 5-year AAA spreads moving up by a basis point to 69 bps levels.

Source: MOSL

October 13, 2010

Liquid, income and equity led to total outflows of Rs. 71,838 crore

Sensex at its 33-month peak; a cycle from 20,000 to 20,000. Investors are anxious, markets are overheated. Mutual fund industry has been bleeding and it remains continuous, in fact certain. Equity funds have been witnessing redemptions; in Sept 2010, equity funds saw its maximum ever redemption amount of Rs. 7,011 crore. In the last 14 months, since the ban of entry load on mutual funds, the outflows have been for 11 times while inflows have been for 3 times. In totality, the redemptions till date since Aug 2009 are Rs. 21,461 crore. Not only equity funds, Balanced Funds too witnessed an outflow of Rs. 414 crore. It is the maximum outflow in Balanced Category in recent years.

Earlier, the fund houses were complaining of low incentives to boost distributors to sell products; now the investors have been redeeming the funds as many fear that there could be a correction in Equity Markets. With many funds reaching new NAV highs, investors preferred trimming their holdings. However, the gross inflows in Equity Funds during the month were the highest since April this year. It was Rs. 5,793 crore in Sept 2010 compared with Rs. 4,928 crore in Aug 2010. Also, the total assets as in Sept 2010 in Equity Category grew to Rs. 1,85,484 crore from Rs. 1,79,200 crore in Aug 2010 mainly on account of rising of equity.

Except Gilt Funds and ETFs, all other categories witnessed net outflows triggering systematic outflows. Liquid/Money Market Funds witnessed the maximum outflow to the tune of (-) Rs. 36,108 crore. Similarly, Income Funds witnessed outflow by Rs. 28,637 crore. Both categories which cater mainly to institutional investors witnessed heavy redemptions due to liquidity deficit in the financial system. Banks, major investors in these funds have also redeemed their investments in Sept 2010. In totality, the total exposure of banks to Mutual Funds as per the RBI estimates have declined from Rs. 59,984 crore as on Aug 27, 2010 to Rs. 33,534 crore as on Sept 24, 2010.

Overall the industry witnessed net outflows of Rs. 71,838 crore due to large redemptions in debt funds.

ELSS, Equity Linked Saving Schemes where investors get benefits for investments up to Rs. 1 lakh under Sec 80C also saw redemptions to the tune of Rs. 270 crore for the sixth consecutive times since April 2010.

Earlier, the fund houses were complaining of low incentives to boost distributors to sell products; now the investors have been redeeming the funds as many fear that there could be a correction in Equity Markets. With many funds reaching new NAV highs, investors preferred trimming their holdings. However, the gross inflows in Equity Funds during the month were the highest since April this year. It was Rs. 5,793 crore in Sept 2010 compared with Rs. 4,928 crore in Aug 2010. Also, the total assets as in Sept 2010 in Equity Category grew to Rs. 1,85,484 crore from Rs. 1,79,200 crore in Aug 2010 mainly on account of rising of equity.

Except Gilt Funds and ETFs, all other categories witnessed net outflows triggering systematic outflows. Liquid/Money Market Funds witnessed the maximum outflow to the tune of (-) Rs. 36,108 crore. Similarly, Income Funds witnessed outflow by Rs. 28,637 crore. Both categories which cater mainly to institutional investors witnessed heavy redemptions due to liquidity deficit in the financial system. Banks, major investors in these funds have also redeemed their investments in Sept 2010. In totality, the total exposure of banks to Mutual Funds as per the RBI estimates have declined from Rs. 59,984 crore as on Aug 27, 2010 to Rs. 33,534 crore as on Sept 24, 2010.

Overall the industry witnessed net outflows of Rs. 71,838 crore due to large redemptions in debt funds.

ELSS, Equity Linked Saving Schemes where investors get benefits for investments up to Rs. 1 lakh under Sec 80C also saw redemptions to the tune of Rs. 270 crore for the sixth consecutive times since April 2010.

On a positive note, Gilt Funds witnessed a net inflow to its kitty. It witnessed a net inflow of Rs. 521 crore. The G-Sec yields have been trading at their high levels mainly on account of RBI’s aggressive monetary policies and high inflationary pressures. Headline Inflation as measured by WPI is set to moderate by the end of this fiscal year. Moreover, liquidity may also improve by Jan-Feb next year. All these factors may bring down G-Sec yields which will benefit these Gilt Funds to the maximum.

In Equity Category, there were 3 NFOs – IDBI Nifty Junior Index Fund; Reliance Small Cap Fund, Reliance Index Fund – Nifty Plan and Sensex Plan which collected a total amount of Rs. 677 crore. Two Ultra Short Term Funds – IDBI Ultra Short Term Fund and Pramerica Ultra Short Term Bond Fund were launched which collected Rs. 597 crore in combine. FMPs continue to rule the industry with a total of 37 new NFOs which collected a total amount of Rs. 7,454 crore. The high short term yields can be attributed to these launches which have caught the attraction of investors.

October 5, 2010

Decoupling - a class example

German DAX Index and India's NSE Nifty 50 are just now at the same numeric value of 6153. In March 2003, DAX was at 2423 point and Nifty was at 934 point. That's what the Decoupling stand for. India's strong consumption story supports it.

German DAX Index and India's NSE Nifty 50 are just now at the same numeric value of 6153. In March 2003, DAX was at 2423 point and Nifty was at 934 point. That's what the Decoupling stand for. India's strong consumption story supports it.September 16, 2010

RBI Mid-Sept Monetary Policy Review – Loans to become dearer

The hawkish global economy recovery coupled with high inflationary pressures forced the Central Bank to raise Policy Rates at the pace faster than the market expectations. The Central Bank, RBI in its Mid-Quarter Monetary Policy Review increased the repo rate and reverse repo rate under LAF.

• Repo Rate and Reverse Repo Rate under Liquidity Adjustment Facility (LAF) increased by 25 bps and 50 bps to 6 per cent and 5 per cent respectively, thus, bringing out the LAF rate corridor to 1 per cent.

• Bank Rate and CRR (Cash Reserve Ration) retained at the same level of 6 per cent each

Domestic Scenario

The RBI stressed on that fact that Inflation has become a kind of concern; even the new index of headline inflation as measured by WPI suggests that the monthly average of WPI inflation for Q1 of 2010-11 under the new series at 10.6 per cent was about 50 bps lower than the rate of 11.1 per cent under the old series. Inflation rates have reached its peak and are most likely to remain at the same level for the next few months. However, Food Inflation continues to move northwards and touched 14 per cent in Aug 2010 as per new series.

Another concern that the RBI documented that the negative real interest rates have been affecting deposit growth rates of banks as savers look for higher returns elsewhere. The RBI wanted deposit growth rates to increase as accordingly the bond supply will be a thorough affair in its weekly auctions without any devolvement which may put pressure on yields. The trend suggests that higher deposit growth rate require higher demands for federal bonds as the bank need to maintain the SLR requirement.

The RBI also indicated that higher than expected realizations on 3G and BMA auctions combined with robust tax revenues have virtually eliminated the risk of the fiscal deficit overshooting its target of 5.5 per cent, even after the additional demand for grants from the Central Government have come up in the Parliament. The Water God, Monsoon has revived the growth prospects in Agriculture which will contribute to good rabi harvest.

Liquidity – from a large surplus to deficit

From a surplus mode, the liquidity entered into a deficit mode after the July Policy review, thus, making the repo rate as the operative policy rate. The current hike will prompt many banks to raise the lending and deposit rates which will sustain the strength of the transmission mechanism.

Global Factors

The RBI remained elusive of global circumstances where the slow recovery has halted many advanced economies to hold their rates further for an extended period. This led to massive inflows into developing economies including India. Moreover, the weak global demand coupled with strong domestic demand has increased the trade deficit and the current account deficit has also been widening. However, Europe has demonstrated remarkable resilience; China too bounced back with industrial production and trade numbers reviving sharply. “Overall, even as the global environment continues to be a cause for caution, the big picture has not worsened significantly since July”, said RBI in a press note.

Need for the hike in Policy Rates

Though the hike in policy rates were expected but by increasing the Reverse Repo Rate by 50 bps, higher than the market expectation of 25 bps, the RBI has used this opportunity to reduce the LAF rate corridor, which will reduce the expected volatility in overnight rates. Moreover, it also wanted to reduce the impact of negative real interest rates which led to savers to move to alternate products giving higher returns.

• Repo Rate and Reverse Repo Rate under Liquidity Adjustment Facility (LAF) increased by 25 bps and 50 bps to 6 per cent and 5 per cent respectively, thus, bringing out the LAF rate corridor to 1 per cent.

• Bank Rate and CRR (Cash Reserve Ration) retained at the same level of 6 per cent each

Domestic Scenario

The RBI stressed on that fact that Inflation has become a kind of concern; even the new index of headline inflation as measured by WPI suggests that the monthly average of WPI inflation for Q1 of 2010-11 under the new series at 10.6 per cent was about 50 bps lower than the rate of 11.1 per cent under the old series. Inflation rates have reached its peak and are most likely to remain at the same level for the next few months. However, Food Inflation continues to move northwards and touched 14 per cent in Aug 2010 as per new series.

Another concern that the RBI documented that the negative real interest rates have been affecting deposit growth rates of banks as savers look for higher returns elsewhere. The RBI wanted deposit growth rates to increase as accordingly the bond supply will be a thorough affair in its weekly auctions without any devolvement which may put pressure on yields. The trend suggests that higher deposit growth rate require higher demands for federal bonds as the bank need to maintain the SLR requirement.

The RBI also indicated that higher than expected realizations on 3G and BMA auctions combined with robust tax revenues have virtually eliminated the risk of the fiscal deficit overshooting its target of 5.5 per cent, even after the additional demand for grants from the Central Government have come up in the Parliament. The Water God, Monsoon has revived the growth prospects in Agriculture which will contribute to good rabi harvest.

Liquidity – from a large surplus to deficit

From a surplus mode, the liquidity entered into a deficit mode after the July Policy review, thus, making the repo rate as the operative policy rate. The current hike will prompt many banks to raise the lending and deposit rates which will sustain the strength of the transmission mechanism.

Global Factors

The RBI remained elusive of global circumstances where the slow recovery has halted many advanced economies to hold their rates further for an extended period. This led to massive inflows into developing economies including India. Moreover, the weak global demand coupled with strong domestic demand has increased the trade deficit and the current account deficit has also been widening. However, Europe has demonstrated remarkable resilience; China too bounced back with industrial production and trade numbers reviving sharply. “Overall, even as the global environment continues to be a cause for caution, the big picture has not worsened significantly since July”, said RBI in a press note.

Need for the hike in Policy Rates

Though the hike in policy rates were expected but by increasing the Reverse Repo Rate by 50 bps, higher than the market expectation of 25 bps, the RBI has used this opportunity to reduce the LAF rate corridor, which will reduce the expected volatility in overnight rates. Moreover, it also wanted to reduce the impact of negative real interest rates which led to savers to move to alternate products giving higher returns.

September 13, 2010

Yields to take cues from Inflation and Policy meet

Highlights:

• The bonds remained jittery throughout the week; however, it settled down at low levels as compared to last week closures.

• The Industrial Output Data as measured by Index of Industrial Production (IIP) rose a more-than expected 13.8 per cent in July 2010, or nearly twice the 7.2 per cent seen in last month.

• Retail Inflation and Food Inflation rose over 15 per cent and 11 per cent, causing a concern for RBI which may hike the rates again.

• The market liquidity remained comfortable with the net absorption of Rs. 27,640 crore under LAF window. However, it would remain in deficit mode going forward.

• The market speculation that the current benchmark paper will be replaced have been put on hold after a Senior Finance Ministry official stated that there is adequate headroom in the current 10-year paper and the bond is expected to last for the entire borrowing in FY11.

View & Recommendations:

• The unexpected factory output at 13.8 per cent plus the high inflation figures may prompt the central bank RBI to revise the policy rates upwards. However, the market has already factored into the 25-bps hike in policy rates.

• Bond yields may soften further in view of global economic environment especially from US i.e. better than expected US Employment data.

• The absence of debt sale in the coming week will keep the demand for debt papers high. The real tone will be set after the mid-quarter policy review this week. Any positive surprise will be greeted with a rally in bond prices. The market is likely to focus on domestic data and policy measures. The policy meet will also review the awaited headline inflation figure due on Sept 14, 2010.

Broader Perspectives:

Bond Front

It is concerned that policy makers are running out of ammunition to control inflation and high factory output is also reigning in strongly; the RBI may go for an upward hike in policy rates. However, the mixed sentiments emanating from global markets are preventing RBI from taking any extreme measures. US President Barack Obama commented that US economy was taking longer than expected time to recover from economic shivers. However, the better-than-expected growth in US employment increased the odds of a fifth interest-rate hike this year.

Bond prices moved up with the 10-year benchmark yield witnessing a drop of 7 bps. The benchmark bond 7.80% 2020 yield nosedived from 7.98 per cent to 7.91 per cent. The comment by the Senior Finance Ministry over the continuance of the current 10-year benchmark bond for the remaining fiscal year 2010-11 boosted the sentiments among traders and investors which lapped the bond to make the prices attractive. He added that the government's preference was to borrow through papers of longer maturity, in order to evenly spread out its outstanding. However, the 8.13% G-Sec 2020 eased only 1 bps to 8.04 per cent. The G-Sec volume was also strong as reported in NDS-OM platform; it showed a daily average of Rs. 12,353 crore over the week. The 1-10 year spread also reported a sharp drop from 168 bps to 149 bps.

Bond Supply

The government auctioned securities worth Rs. 11,000 crore last week. The bonds auctioned were the 7.17% 2015 for Rs. 4,000 crore, the 8.13% 2022 for Rs. 4,000 crore and the 8.26% 2027 for Rs. 3,000 crore respectively. The cut-offs were in line with the market expectations which came in at 7.69 per cent, 8.02 per cent and 8.35 per cent. Five State Governments namely Maharashtra, Punjab, Tamil Nadu, Uttar Pradesh and West Bengal conducted the auction of their State Development Loans for combined amount of Rs. 5,300 crore on Sept 07, 2010. Their cut-off yields were in the range of 8.29 per cent to 8.41 per cent.

Liquidity

The liquidity was comfortable throughout the week as measured by bids for Repo and Reverse Repo auctions in Liquidity Adjustment Facility (LAF). The net absorption amount was Rs. 27,640 crore for this week. This week, there won’t be any auction which will ease off the liquidity. However, the advance tax outflow to the tune of Rs. 50,000 will put the liquidity in deficit mode. The average Call and CBLO rates dropped to 4.65 per cent and 4.28 per cent from 4.77 per cent and 4.75 per cent respectively over the week.

Corporate Bonds

Corporate bonds’ yields fell over the week. The 10-year AAA bond ended at a yield of around 8.71 per cent compared to 8.75 per cent. However, the 1-year bond hardened by 15 bps to 7.95 per cent from 7.80 per cent a week earlier. In the primary market, EXIM Bank raised Rs. 100 crore with 5-year paper and another Rs. 100 crore with 10-year paper with an annualized yield of 8.45 per cent and 8.68 per cent.

• The bonds remained jittery throughout the week; however, it settled down at low levels as compared to last week closures.

• The Industrial Output Data as measured by Index of Industrial Production (IIP) rose a more-than expected 13.8 per cent in July 2010, or nearly twice the 7.2 per cent seen in last month.

• Retail Inflation and Food Inflation rose over 15 per cent and 11 per cent, causing a concern for RBI which may hike the rates again.

• The market liquidity remained comfortable with the net absorption of Rs. 27,640 crore under LAF window. However, it would remain in deficit mode going forward.

• The market speculation that the current benchmark paper will be replaced have been put on hold after a Senior Finance Ministry official stated that there is adequate headroom in the current 10-year paper and the bond is expected to last for the entire borrowing in FY11.

View & Recommendations:

• The unexpected factory output at 13.8 per cent plus the high inflation figures may prompt the central bank RBI to revise the policy rates upwards. However, the market has already factored into the 25-bps hike in policy rates.

• Bond yields may soften further in view of global economic environment especially from US i.e. better than expected US Employment data.

• The absence of debt sale in the coming week will keep the demand for debt papers high. The real tone will be set after the mid-quarter policy review this week. Any positive surprise will be greeted with a rally in bond prices. The market is likely to focus on domestic data and policy measures. The policy meet will also review the awaited headline inflation figure due on Sept 14, 2010.

Broader Perspectives:

Bond Front

It is concerned that policy makers are running out of ammunition to control inflation and high factory output is also reigning in strongly; the RBI may go for an upward hike in policy rates. However, the mixed sentiments emanating from global markets are preventing RBI from taking any extreme measures. US President Barack Obama commented that US economy was taking longer than expected time to recover from economic shivers. However, the better-than-expected growth in US employment increased the odds of a fifth interest-rate hike this year.

Bond prices moved up with the 10-year benchmark yield witnessing a drop of 7 bps. The benchmark bond 7.80% 2020 yield nosedived from 7.98 per cent to 7.91 per cent. The comment by the Senior Finance Ministry over the continuance of the current 10-year benchmark bond for the remaining fiscal year 2010-11 boosted the sentiments among traders and investors which lapped the bond to make the prices attractive. He added that the government's preference was to borrow through papers of longer maturity, in order to evenly spread out its outstanding. However, the 8.13% G-Sec 2020 eased only 1 bps to 8.04 per cent. The G-Sec volume was also strong as reported in NDS-OM platform; it showed a daily average of Rs. 12,353 crore over the week. The 1-10 year spread also reported a sharp drop from 168 bps to 149 bps.

Bond Supply

The government auctioned securities worth Rs. 11,000 crore last week. The bonds auctioned were the 7.17% 2015 for Rs. 4,000 crore, the 8.13% 2022 for Rs. 4,000 crore and the 8.26% 2027 for Rs. 3,000 crore respectively. The cut-offs were in line with the market expectations which came in at 7.69 per cent, 8.02 per cent and 8.35 per cent. Five State Governments namely Maharashtra, Punjab, Tamil Nadu, Uttar Pradesh and West Bengal conducted the auction of their State Development Loans for combined amount of Rs. 5,300 crore on Sept 07, 2010. Their cut-off yields were in the range of 8.29 per cent to 8.41 per cent.

Liquidity

The liquidity was comfortable throughout the week as measured by bids for Repo and Reverse Repo auctions in Liquidity Adjustment Facility (LAF). The net absorption amount was Rs. 27,640 crore for this week. This week, there won’t be any auction which will ease off the liquidity. However, the advance tax outflow to the tune of Rs. 50,000 will put the liquidity in deficit mode. The average Call and CBLO rates dropped to 4.65 per cent and 4.28 per cent from 4.77 per cent and 4.75 per cent respectively over the week.

Corporate Bonds

Corporate bonds’ yields fell over the week. The 10-year AAA bond ended at a yield of around 8.71 per cent compared to 8.75 per cent. However, the 1-year bond hardened by 15 bps to 7.95 per cent from 7.80 per cent a week earlier. In the primary market, EXIM Bank raised Rs. 100 crore with 5-year paper and another Rs. 100 crore with 10-year paper with an annualized yield of 8.45 per cent and 8.68 per cent.

September 2, 2010

IRDA regulations – Policyholders to be benefitted

The recent spat between IRDA, the Insurance Regulator and SEBI, the Capital Market Regulator created an outcry in the market with each party holding its supremacy over the much sought and widely circulated insurance product, Unit Linked Insurance Products (ULIPs) in India. The Government of India in quick solution passed an ordinance to support the IRDA regulation over ULIPs ending the market speculation that SEBI might make Ulips in line with Mutual Funds.

Fresh from its victory in the regulatory turf war over ULIPs, the IRDA announced a set of regulations. With the expansion of insurance sector and more innovative insurance products, particularly Unit Linked Insurance Products (ULIPs) entering into Life Insurance products list, IRDA has been sensitive to the changing scenario. In the past, IRDA has come out with various steps to bring in changes in the regulatory framework to address various concerns of the policyholders.

IRDA in a note stipulated that insurers must provide the prospect/policyholder all relevant information regarding amounts deducted towards various charges for each policy year so that the prospect could take an informed decision. IRDA also raised the concerns of mis-selling and Distance Marketing which require guidelines from the insurance regulator. Further, IRDA set up an exclusive Customer Affairs Department that focuses on consumer related issues and initiatives including grievance redressal and consumer education through Insurance Awareness Campaigns. It is perhaps the most important step in the interests of policyholders.

Recent Regulatory Proposals

ULIPs are hybrid instruments that combine elements of mutual funds and insurance. In most cases, the insurance amount is capped to 5-times of initial insurance premium. Recently, IRDA came out with guidelines governing ULIPs – how such products are sold/bought; how ULIPs can be better financial instruments for providing risk coverage and many more. Some of the ULIPs related regulations are as given below:

1) Level Paying Premium

All regular premium /limited premium ULIPs shall have uniform/level playing premiums. Any additional payments shall be treated as single premium for the purpose of insurance cover.

2) Compulsory Cover

Currently there are a number of ULIPs schemes where there is maximum insurance cover up to five times of the premium paid or no insurance cover. Now it has been recommended that the life insurance component has to be at least 10 times the premium paid for policies up to 10 years and at least 1.05 times the annual premium for policies of 20 years and above.

3) Lock in Period increased to Five Years

IRDA has increased the lock-in period for all ULIPs from three years to five years, including top-up premiums, thereby making them long term financial instruments which basically provide risk protection.

4) Minimum Premium Paying term of Five Years

All limited premium ULIPs, other than single premium products shall have premium paying term of at least five years

5) Even Distribution of Charges

Charges on ULIPs are mandated to be evenly distributed during the lock-in period, to ensure that high front ending of expenses is eliminated.

6) Pension Plans to have Guaranteed Return

As regards pension products, all ULIP pension/annuity products shall offer a minimum guaranteed return of 4.5% per annum or as specified by IRDA from time to time. This will protect the life time savings for the pensioners, from any adverse fluctuations at the time of maturity.

7) Rationalization of Cap on Charges

With a view to smoothen the cap on charges, the capping has been rationalized to ensure that the difference in yield is capped from the 5th onwards. This will not only reduce the overall charges on these products, but also smoothen the charge structure for the policyholder.

Though these regulations have been rolled out for the benefit of common policyholders, the insurers will have a level playing field with other players and will benefit in the long run.

September 1, 2010

Yields to fall – Focus on Income Funds

Inflation has started coming down. WPI, the official figure for measure of Inflation came down to 9.97 per cent, 0.03 per cent shy of two digits. The RBI concern on ballooned inflation, a shift of focus from growth to inflation led to a series of monetary policy measures this year, already four times witnessed. More worrisome is the fact that the inflation is no longer food prices driven; in fact it has become more generalized. Non-food inflation has risen from almost zero level in Nov 2009 to 10.9 per cent in June 2010, contribution 70 per cent to inflation.

The bond yields rose abruptly in India, however, the bond yields came down globally. For the first time in its history, the 10-year Indian and US bond yields are facing a divergent state.

The G-Sec markets witnessed hardening of yields in July and Aug 2010. The 10-year G-Sec Bond and Short Term Bonds’ yields have spiked in the recent past; which we believe that they may go up further projected the advance tax outflows in Mid September. The short term yields (1-year CD and CP) have already spiked by 200 bps in the last 3 months. The benchmark bond 7.80 per cent 2020 has already touched 8.08 per cent, currently hovering at 8.03%. It touched its four months high since May 2010. The RBI is still not comfortable with the inflation figures and the market opines that it may go with further rate hikes in the upcoming Monetary Policy meet due in mid-Sept.

We believe that the G-Sec yields in long term will follow its logical course of softening. The reasons are:

• Softening of inflation in coming months

• Improvement in Government revenues in the form of improved tax inflows, 3G and WIMAX auctions

• Reduction in fiscal deficit, if the excess revenue is used efficiently

• Spread in the Repo rate and 10-year G-Sec rate (already at multiple year high) should reduce

• Liquidity is bound to improve; temporarily we might witness liquidity deficiency in the system

• For the first time since 2002, interest rates in India are divergent to US yields (Check the above table)

Since US government continues to follow an expansionary monetary policy to revive growth, the Fed has kept its interest rates abysmal low for another extended period. However, in India, RBI has shifted its focus from good GDP/IIP growth to inflation management; therefore, we witnessed tightening of monetary policy. When inflation comes under control over next few months, bond yields (long dated bonds) will follow its logical course of softening. For those seeking to ride the yield curve at the longer end which could potentially ease in the 2nd half, we would recommend allocations to Income Fund having high average maturity. In the above stated scenario, the income funds stand to benefit with a time horizon of 12 to 18 months.

The bond yields rose abruptly in India, however, the bond yields came down globally. For the first time in its history, the 10-year Indian and US bond yields are facing a divergent state.

The G-Sec markets witnessed hardening of yields in July and Aug 2010. The 10-year G-Sec Bond and Short Term Bonds’ yields have spiked in the recent past; which we believe that they may go up further projected the advance tax outflows in Mid September. The short term yields (1-year CD and CP) have already spiked by 200 bps in the last 3 months. The benchmark bond 7.80 per cent 2020 has already touched 8.08 per cent, currently hovering at 8.03%. It touched its four months high since May 2010. The RBI is still not comfortable with the inflation figures and the market opines that it may go with further rate hikes in the upcoming Monetary Policy meet due in mid-Sept.

We believe that the G-Sec yields in long term will follow its logical course of softening. The reasons are:

• Softening of inflation in coming months

• Improvement in Government revenues in the form of improved tax inflows, 3G and WIMAX auctions

• Reduction in fiscal deficit, if the excess revenue is used efficiently

• Spread in the Repo rate and 10-year G-Sec rate (already at multiple year high) should reduce

• Liquidity is bound to improve; temporarily we might witness liquidity deficiency in the system

• For the first time since 2002, interest rates in India are divergent to US yields (Check the above table)

Since US government continues to follow an expansionary monetary policy to revive growth, the Fed has kept its interest rates abysmal low for another extended period. However, in India, RBI has shifted its focus from good GDP/IIP growth to inflation management; therefore, we witnessed tightening of monetary policy. When inflation comes under control over next few months, bond yields (long dated bonds) will follow its logical course of softening. For those seeking to ride the yield curve at the longer end which could potentially ease in the 2nd half, we would recommend allocations to Income Fund having high average maturity. In the above stated scenario, the income funds stand to benefit with a time horizon of 12 to 18 months.

August 10, 2010

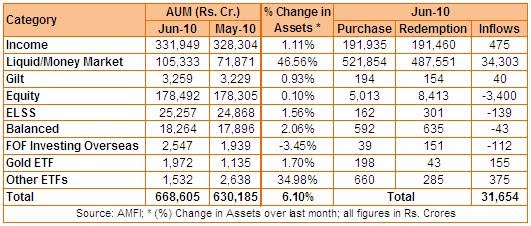

Equity outflows continue; industry added Rs. 31,654 crore

Mutual Fund industry saw a temporary relief after witnessing outflows in last two months consecutively. In July 2010, the industry saw a net inflow of Rs. 31,654 crore to its kitty mainly on account of net inflow of Rs. 34,303 crore in Liquid/Money Market category. On the other hand, the total AUM increased to Rs. 6.68 lakh crore, a rise of Rs. 38,420 crore or 6.10 per cent over the last month figure. All categories except FOF Investing Overseas reported an increase in its net AUM. While Income Funds comprising 50 per cent of total AUM reported a meager increase of 1.11 per cent in its AUM, Liquid/Money Market Fund category reported an increase of 46.56 per cent. The latest AUM figures for Income and Liquid/Money Market Fund stand at Rs. 3,31,949 crore and Rs. 1,05,333 crore respectively. The Other ETFs category shows a dramatic increase in AUM after Motilal Oswal Mutual Fund successfully closed its maiden fundamentally modified ETF MOSt Shares M50 with a total AUM of Rs. 236 crore. It has a total AUM of Rs. 1,532 crore, an increase of Rs. 397 crore other its last month figure. The Diversified Equity category showed a negligible increase of 0.10 per cent to Rs. 1,78,492 crore. Other categories too moved up albeit marginally.

The Equity Diversified Fund category saw a major redemption having a total outflow of Rs. 8,413 crore against an inflow of Rs. 5,013 crore, thus, a net redemption of Rs. 3,400 crore. The equity markets have already touched their February 2008 level and investors have become cautious of overheat going in the equity market as they fear a correction from this level. Moreover, some investors who were sitting at their investment since 2007 had also redeemed their money. Hence mutual funds booked profit to meet investors’ redemption pressures. As per the latest SEBI figures, Mutual Funds had net sale of Rs. 4,405 crore in July 2010.

The Liquid/Money Market saw the maximum inflow of Rs. 34,303 crore mainly on account of switch outs from Income/Ultra Short Term Funds to Liquid Funds. After the introduction of new MTM ruling on debt securities having average maturities more than 91 days, the Ultra Short Term Funds were the worst hit. Corporate fears that it will bring volatility to the funds which will bring down the returns. They eventually shifted to Liquid Funds or redeemed their investments. The Income category saw a net inflow of Rs. 475 crore only.

In other categories, ELSS saw a new outflow of Rs. 139 entering into fourth month having outflows consecutively month-on-month. Balanced Funds too saw an outflow of Rs. 43 crore continuing its last month losing streak. However, the industry has been witnessing a major shift since last few months from active funds to passive funds. ETFs which cater to passive funds category have seen a substantial increase in inflows. The Gold ETF and other ETFs category added Rs. 155 crore and Rs. 375 crore respectively.

The month also saw the launch of 7 open-ended NFOs and 15 close-ended NFOs (mainly FMPs). The 15 close-ended income funds collected Rs. 2,444 crore from the market while the 3 open-ended close ended funds collected Rs. 840 crore. The income category NFOs were Axis Income Saver, Canara Robeco InDiGo Fund and Peerless Income Plus Fund. The 2 open-ended Equity NFOs, mainly Mirae Asset Emerging Bluechip Fund and SBI PSU Fund collected a total of Rs. 705 crore. In other ETFs category, Motilal Oswal MOSt Shares M50 ETF collected Rs. 236 crore in its maiden NFO.

The Equity Diversified Fund category saw a major redemption having a total outflow of Rs. 8,413 crore against an inflow of Rs. 5,013 crore, thus, a net redemption of Rs. 3,400 crore. The equity markets have already touched their February 2008 level and investors have become cautious of overheat going in the equity market as they fear a correction from this level. Moreover, some investors who were sitting at their investment since 2007 had also redeemed their money. Hence mutual funds booked profit to meet investors’ redemption pressures. As per the latest SEBI figures, Mutual Funds had net sale of Rs. 4,405 crore in July 2010.

|

| Table: Mutual Fund Asset Growth |

In other categories, ELSS saw a new outflow of Rs. 139 entering into fourth month having outflows consecutively month-on-month. Balanced Funds too saw an outflow of Rs. 43 crore continuing its last month losing streak. However, the industry has been witnessing a major shift since last few months from active funds to passive funds. ETFs which cater to passive funds category have seen a substantial increase in inflows. The Gold ETF and other ETFs category added Rs. 155 crore and Rs. 375 crore respectively.

The month also saw the launch of 7 open-ended NFOs and 15 close-ended NFOs (mainly FMPs). The 15 close-ended income funds collected Rs. 2,444 crore from the market while the 3 open-ended close ended funds collected Rs. 840 crore. The income category NFOs were Axis Income Saver, Canara Robeco InDiGo Fund and Peerless Income Plus Fund. The 2 open-ended Equity NFOs, mainly Mirae Asset Emerging Bluechip Fund and SBI PSU Fund collected a total of Rs. 705 crore. In other ETFs category, Motilal Oswal MOSt Shares M50 ETF collected Rs. 236 crore in its maiden NFO.

Source: MOSL Mutual Fund Desk

July 9, 2010

Exchange Traded Funds (ETFs) Innovations – MOSt Shares M50 ETF

Global Journey

ETFs have travelled a long distance since its inception in 1993 in USA. It took 7 years (from 1993 – 2000) to get it widely accepted among investors. Once it drew attention from investors, it grew leap and bound; the global ETF assets has reached an all time high of US $ 1.03 trillion as on March 2010 from an estimated US $ 463 million in 1993, clocking a CAGR of 56 per cent. On US Exchanges, 11 out of top 25 volume leaders/stocks are ETFs. Some of the top volume leader ETFs is SPDRs, iShares MSCI Brazil Index, Ultra Short Russel2000 ProShares, etc. These ETFs account for 78 per cent of total volume out of top 25 traded stocks on US Stock Exchanges. It was less than 25 per cent 10 years back.

Indian Journey

Not very old in India, ETFs started its journey in 2001 after Benchmark AMC forayed into this unique proposition. Since then, the ETFs grew by leap and bound. The domestic ETF assets grew from Rs. 7 crore in 2001 to Rs. 3,203 crore as on May 31, 2010. However, the main course of action in ETFs got intensified in the recent bull period. Indian equities component of Global Emerging Markets ETFs account for US $ 5.5 billion of AUM while the domestic equity ETFs now account for US $ 0.5 billion. Overall, over the past year, around 20 per cent of the net inflows into the Indian market have come from ETFs, thereby, ETFs a very significant component of Indian fund flows.

Is ETFs good for investors?

The global historical data suggests that the fund managers have not been able to beat the benchmarks constantly over a longer period. In efficient market scenario, the active funds find difficulty in beating their benchmarks. So, it is always preferable for investors to look for a product which provide a decent return, at least comparable to its benchmark with bounty of other benefits such as tax efficiency, low expense ratios.

ETFs are pools of stocks, bonds or in a few instances other types of investments such as Gold that you can trade like stocks. ETFs tend to have very low annual expenses – much lower than the actively managed funds. Moreover, ETFs are high tax efficient i.e. they tend to minimize distributions, which will drive down your post-tax returns. ETFs are listed on stock exchanges and can be bought and sold like any other company share.

Product Innovations

Innovation is the key to success. For now, at least, all ETFs are an index fund which mirrors an index or a benchmark, unlike actively managed funds whose managers try to beat the market. There have been talk of companies bringing out actively managed ETFs, but so at least in India, it has not been manufactured. Currently, in India, the underlying for ETFs are Index, Sector, Money Market Instruments, Arbitrage etc. One more type to add in the basket of innovated products is actively managed ETF – MOSt Shares M50 ETF, the first of its kind in India, launched by Motilal Oswal Mutual Fund.

Passively-managed ETFs follows its index and invest in the same proportion as of its index while actively-managed ETFs follow their own fundamentally defined rules.

ETFs have travelled a long distance since its inception in 1993 in USA. It took 7 years (from 1993 – 2000) to get it widely accepted among investors. Once it drew attention from investors, it grew leap and bound; the global ETF assets has reached an all time high of US $ 1.03 trillion as on March 2010 from an estimated US $ 463 million in 1993, clocking a CAGR of 56 per cent. On US Exchanges, 11 out of top 25 volume leaders/stocks are ETFs. Some of the top volume leader ETFs is SPDRs, iShares MSCI Brazil Index, Ultra Short Russel2000 ProShares, etc. These ETFs account for 78 per cent of total volume out of top 25 traded stocks on US Stock Exchanges. It was less than 25 per cent 10 years back.

Indian Journey

Not very old in India, ETFs started its journey in 2001 after Benchmark AMC forayed into this unique proposition. Since then, the ETFs grew by leap and bound. The domestic ETF assets grew from Rs. 7 crore in 2001 to Rs. 3,203 crore as on May 31, 2010. However, the main course of action in ETFs got intensified in the recent bull period. Indian equities component of Global Emerging Markets ETFs account for US $ 5.5 billion of AUM while the domestic equity ETFs now account for US $ 0.5 billion. Overall, over the past year, around 20 per cent of the net inflows into the Indian market have come from ETFs, thereby, ETFs a very significant component of Indian fund flows.

Is ETFs good for investors?

The global historical data suggests that the fund managers have not been able to beat the benchmarks constantly over a longer period. In efficient market scenario, the active funds find difficulty in beating their benchmarks. So, it is always preferable for investors to look for a product which provide a decent return, at least comparable to its benchmark with bounty of other benefits such as tax efficiency, low expense ratios.

ETFs are pools of stocks, bonds or in a few instances other types of investments such as Gold that you can trade like stocks. ETFs tend to have very low annual expenses – much lower than the actively managed funds. Moreover, ETFs are high tax efficient i.e. they tend to minimize distributions, which will drive down your post-tax returns. ETFs are listed on stock exchanges and can be bought and sold like any other company share.

Product Innovations

Innovation is the key to success. For now, at least, all ETFs are an index fund which mirrors an index or a benchmark, unlike actively managed funds whose managers try to beat the market. There have been talk of companies bringing out actively managed ETFs, but so at least in India, it has not been manufactured. Currently, in India, the underlying for ETFs are Index, Sector, Money Market Instruments, Arbitrage etc. One more type to add in the basket of innovated products is actively managed ETF – MOSt Shares M50 ETF, the first of its kind in India, launched by Motilal Oswal Mutual Fund.

Passively-managed ETFs follows its index and invest in the same proportion as of its index while actively-managed ETFs follow their own fundamentally defined rules.

July 2, 2010

MOSt Shares M50 – Is it another offer in the crowd?

Among the above captioned NFOs, all the NFOs were more or less similar to the existing plans offered by another fund houses; I found a unique offer by Motilal Oswal AMC with its maiden NFO MOSt Shares M50 ETF. Though the ETF concept is new in India and has not been well received by investors yet, ETFs are on high. Historically, it has grown exceptionally even in intermittent market. Let me give out in detail why MOSt Shares M50 ETF is unique and investors’ friendly.

Product Features

As claimed by Motilal Oswal Mutual Fund, MOSt Shares M50 ETF is India’s 1st fundamentally weighted ETF based on the S&P CNX Index (Nifty). Logically, it is the remixed version of Nifty 50. The fund house has created its own basket “MOSt 50 Basket”, intellectually owned by MOAMC and managed by India Index Services & Products Ltd. (IISL). The weights of stocks in MOSt 50 Basket will be decided by their pre-defined methodology based on stock’s fundamentals (ROE, Net Worth, Retained Earnings and Valuation).

The fund aims to generate investment returns with minimal costs and active investment style. With no entry and exit load, the investors get another opportunity in terms of liquidity. The fund manager will invest 95-100% of the money in MOSt 50 basket and the exposure to fixed income and money market instruments along with cash call will be restricted to 0-5% of the total money invested.

Investment Strategy

The fund has reworked the weights of stocks in Nifty based on its own defined fundamentals such as Return on Equity, Net Worth, Retained Earnings and Price. They have designed the capital allocation strategy of the MOSt 50 basket to reduce the risk associated with price volatility of individual constituents. The table 1 defines the basket classification of MOSt 50 Basket.

So, some of the companies will be more dominant than others based on the current methodology.

So, some of the companies will be more dominant than others based on the current methodology. Back Testing

Should you buy?

As far as the ETF story is going on, it has been building up in India. People have started recognizing the importance of ETFs as fund managers have failed to outperform the benchmarks over a longer period. Moreover, this new ETFs, also called as active ETF scored over others and provide uniqueness in terms of simplicity and maximization of returns over a longer period.

June 22, 2010

Life Insurance – A Distant Dream for Indians

India, a home to 1.15 billion people and the world’s second largest population stands abysmally low in terms of social security and human needs measures. Since independence, the Government of India introduced many measures to improve the economic conditions of this country. This included various social security schemes, the prominent being ESIC and EPFO followed by some recent measures such as MGNREGA (Mahatma Gandhi National Rural Employment Guarantee Act), National Rural Health Mission etc. The history of Insurance in India dates back to British colonial period, early 19th century. Since then, a lot of reforms came in existence, particularly for Life Insurance. Despite all measures, the penetration of Insurance is still ranked the lowest amongst other countries.

India is an under-insured country and the insurance penetration level stands abysmally low at 2 per cent of the population, the general insurance penetration stands at 0.6 per cent only. With a vast population of 1.15 billion, there is an immense opportunity that needs to be tapped. An estimated 80 per cent of the Indian population is without Life, Non-Life and Health insurance. However, the Indian Insurance industry is poised to grow robustly with a clear path set along the growth trajectory. In terms of total business, the Indian Life Insurance industry has grown from US $ 8.87 billion in Fiscal Year 2005-06 to US $ 41 billion as on Jan 2010, thus, giving an absolute increase of 362 per cent. In an average, the industry has been growing at a rapid pace of 30 – 34 per cent annually, as per Life Insurance Council. LIC, being the earliest player and set up under the Life Insurance Act in 1956 has played a dominant role in spreading its wings across all nooks and corner of India. However, the entry of private insurance players changed the dynamics of Indian Insurance industry.

As regard to the FDI being capped to 26 per cent in Life Insurance, it created an additional opportunity for foreign players who have been looking to tap the untapped insurance potential in India. The total FDI being routed to India under FDI to Insurance is US $ 525.6 billion. The government is keen to reintroduce the Insurance Bill which proposes to increase the FDI level to 49 per cent from the current level of 26 per cent.

But the question arises, why India is still tagged as Under Insurance industry? Have the government not done enough to increase the penetration level to all corners of India?

Why Insurance is sold in India?

Insurance policies are sold in India unlike its developed counterparts where it is sought after. No doubt, the major reason is poverty and low level of penetration in rural areas. The major population which is largely based in rural areas has low level of financial knowledge. Since, majority of India’s population is living below the poverty level (BPL), they are more interested in living their livelihoods instead of protecting their futures against any mishaps. Moreover, the Government of India does not run any social security schemes on its own unlike in other developed countries which contribute on their behalf. The lack of a proper path hampers the penetration level in insurance. One of the tools to measure the insurance development is per capital spending on insurance i.e. insurance density. Based on this measure, India ranks among the lowest spending nations in Asia in respect of purchasing insurance. Another factor that has been slowing the improvement of insurance density in India is its relatively high population growth rate.

The low income level (average per capital income being at Rs. 44,345 in 2009-10) also deters individuals to ask for insurance as a product to safeguard their futures. Moreover, insurance is not compulsory in India except Motor Third Party Liability. There is no other compulsory insurance in India. In a nut shell, the awareness is poor because insurance was not sold for years – it was bought. However, the mushrooming of private insurers has helped in a big way to push insurance products. Apart from the usual agent-client relationships, these insurers have been using new innovative measures such as Direct Marketing, Digital Marketing etc. Since Mobile has reached deeply in every nook and corner of India, insurers have been using it in a big way to push products.

What the government has done to boost Insurance in India?

• FDI up to 26 per cent permitted under the automatic route subject to obtaining a license from the Insurance Regulatory Development Authority (IRDA)

• Private insurance players have been allowed into the Insurance business; earlier it was dominated by LIC

• Set up of Insurance Regulatory Development Authority (IRDA) to regulate the insurance industry

• Set up of Foreign Players in conjugation with the domestic players

• Defining new rural business commitments in terms of number of life insurance policies sold and total premium collected, thus, asking allowing life insurance companies to set up their shops in rural and untapped areas

Entry of Private Players in Insurance Business

After the Government of India (GoI) liberalized the insurance sector in March 2000 with the passage of the Insurance and Regulatory Development Authority (IRDA) bill, it allowed the setting up of private and foreign insurance players in 2000. As a result, the total number of Life Insurers increased to 23 as of April 2010, as per IRDA report. The private players in partnership with foreign players brought new dimensions in the industry along with technological know-how, thus, reducing the operational costs and bringing new efficiency in the industry. The scaling up of private insurers reduced the market share of LIC India which forced them to overhaul their set up and its way of functioning. Entry of private insurance players brought alternative distribution channels to suit customers’ needs. So, the industry has moved from the typical meeting between the customer and insurance agent as seen earlier to new technology. New companies are emphasizing on speed, convenience and ease of transactions. Though there have been some mis-selling being reported, it is the regulatory loopholes which they have been exploiting and in the time to come, it will disappear gradually. IRDA has announced a series of regulations to regulate the insurance industry and also improved the solvency ratio, a measure to test the robustness and strength of Insurance Company. The insurance sector is set to witness a sea change in the way the businesses were traditionally done, with new innovative products, distribution network etc. Insurance players have also been experimenting direct marketing plans and have been successful too, to some extent.

Scope of Private Insurers in future